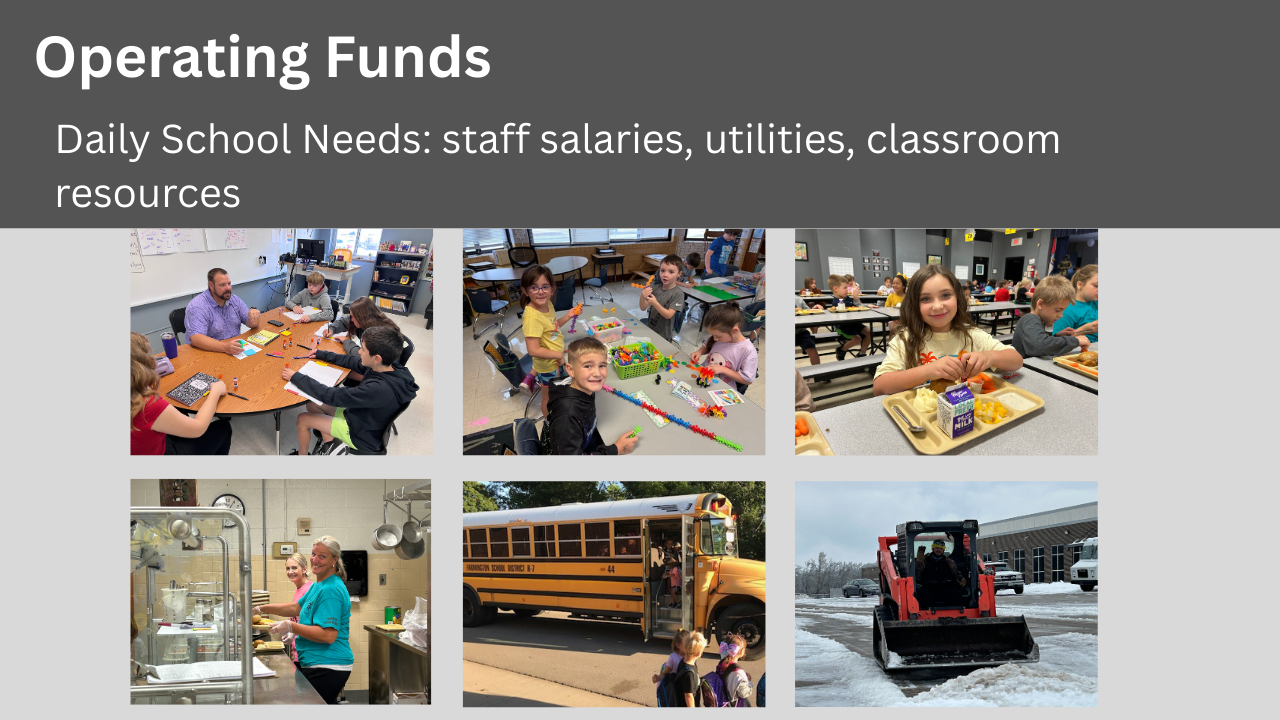

How School Funds Are Used

In Missouri, public school finances are broken into separate funds for clarity and legal compliance primarily:

Budget Planning & Projections

Budget planning is the process of deciding how the district will spend money in the coming year.

Projections are educated forecasts of:

Future revenues

Future expenses

Reserve levels

Financial risks

Think of it as a multi-year financial weather forecast for the district.

Annual Secretary of the Board Report (ASBR)

The Annual Secretary of the Board Report (ASBR) is the official, year-end financial report every Missouri public school district must file with the state.

Think of it as the district’s financial “report card” for the year showing exactly where money came from, where it went, and what’s left.

Audit Reports

A school district audit is an independent, third-party review of the district’s finances to confirm that:

Money was spent legally

Financial statements are accurate

Internal controls are working

State and federal rules were followed

The auditors do not work for the district. They work for the district patrons to ensure that the district is maintaining financial fidelity.

Think of it as a financial inspection, not a performance review and not a budget redo.

Who Requires the Audit

Missouri law requires:

Every public school district to be audited annually

The audit to be performed by a licensed independent CPA firm

The completed audit to be submitted to DESE

Quarterly Financial Reports

Brief explanation goes here

Financial Policies

Last Updated: January 2026